Green Media News sat down with Georgios Stathousis, Associate Director at FutureBridge, to learn more about his vision for shifting to a more circular economy in order to meet climate change goals.

Tell us a little bit about you and your background:

I’m Greek, born and raised in Athens. But over the last decade, I’ve been living in the UK, Netherlands and other countries. I’ve studied economics in Athens and finance in London, driven by my desire to understand how markets work – and what’s the reason why when they don’t work.

I was fortunate to join the automotive industry in a period of dramatic change, which creates big opportunities for new mobility business models and innovative technologies in electrification and autonomy, but also requires forward thinking to shape new customer experiences.

What motivates me is the urgency to shift to sustainability and circular mobility to meet climate change goals through approaches that incentivize individual contribution and coordinate collective action. I also enjoy combining my economics background with my passion for technology to develop growth strategies and build new services around circular mobility, AI and big data.

With regards to my professional background, I have a decade and a half of experience in research and advisory on advanced automotive technologies, from autonomous driving to electrification and shared mobility. I have worked across the industry supply chain, from carmakers to consulting and market research firms.

At Auto2x, I led research on commercialisation roadmaps of cutting-edge technologies and their impact on the competitive landscape to design products and services for carmakers and suppliers.

I supported Jaguar Land Rover’s strategy, technology and commercial roadmap in Advanced Driver Assistance Systems and Autonomous Driving by providing expertise in technology innovation, the evolution of the regulatory landscape, competitor plans and consumer needs.

At FutureBridge, I head up the mobility research products and advise global carmakers, suppliers, and oil & gas majors on the future of automotive technologies, markets and winning business models.

Some of the key areas I’m focused on are:

– Techno-commercial roadmaps for the transition to Level 4-Automated Driving for private cars and robo-services;

– Next-gen technologies for the Cockpit of the Future: Empathetic Human Machine Interface, Emotional Intelligence, Voice-AI, touch-less interfaces;

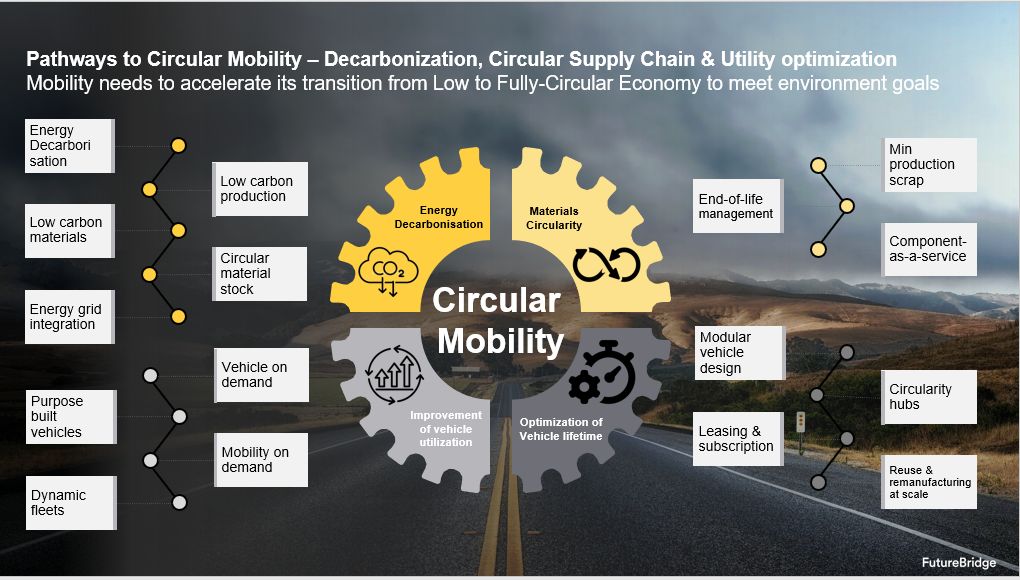

– How to accelerate the pathways to Circular Mobility: beyond decarbonization to materials circularity and optimization of vehicle utilization;

– The future of Sustainable propulsion: fuel-agnostic strategies, Electric powertrains, batteries, hydrogen, and charging infrastructure;

– Inflection points for No-ownership: MaaS, AMoD, VaaS, micro-mobility and new mobility business models.

What is a fun fact about you?

I’m passionate about cars and automotive technology, however, I’m a big believer in the benefits of shared mobility, especially for sustainability. To put it simply, I choose not to own a vehicle but use car-sharing, ride-hailing, and multi-modal transport for my urban commute.

This concept of “usage” instead of “ownership” might come as a surprise to some. Especially, when they seek advice on which electric car is better to “buy”.

Why do you think climate change and sustainability is such an important topic today?

Because we are running out of time to take decisions about de-fossilisation that can alter the course of climate change. What’s more because there is lack of coordination of the action required to have impact.

But there are positive signals as well, such as technological innovation, sustainability regulation and growing consumer sentiment – it’s just not moving fast enough. Let me explain my views on sustainability in more detail using the automotive industry as the use case.

To better understand how to transition to Sustainable Mobility, we need to define Sustainability because there is a misconception that it’s all about electric cars. Sustainable Mobility is a combination of strategies that are interrelated and should be pursued in parallel to progress from Linear Mobility to Circular Mobility. These strategies are de-fossilization (from vehicles to supply chain), supply chain circularity, and optimization of the utilization of vehicles throughout their lifecycle.

A lot has been written about electrification and CO2 emission reduction in transport but energy decarbonization alone, through the shift to electrified powertrains, will not be enough to achieve net-zero CO2 emissions, even if vehicles are manufactured and powered by green electricity. Sustainability expands beyond just electrification. Materials Circularity is needed which focuses on the use of 100% renewable and recyclable materials to enable energy resource recovery and close material loops. Also, Improvement of vehicle utilization and optimization of vehicle lifetime are crucial.

Today, the Mobility market is at a Low state of Circularity.

Energy decarbonization is still at nascent stages. Internal Combustion Engines (Gasoline and Diesel) still maintain the lion’s share across major car markets. More than 75% share in new car sales in China and 53% share in Western Europe in H1 2022. Electrification of the powertrain mix is still in its infancy. Electric car penetration rose to 24% in China in H1 2022, vs. 20% in Europe and just 6% in the US. Green steel and aluminum are not yet prevalent for low-carbon production, but players have started introducing them into vehicle production.

In terms of Materials Circularity, the supply chain is progressing from Linear to include production scrap looping. Battery recycling and 2nd life present new opportunities but still face challenges. New business models for improved Utilization of vehicles are gaining traction, such as car subscriptions, on-demand mobility incl. as ride-hailing and car-sharing but are still niche offerings. Private vehicle ownership is still prominent and vehicle ownership remains high.

Exponential focus is needed across the automotive industry, policymakers, and consumers in the next few years to move from today’s Low Circularity (2021) to Moderate and Full Circularity. To accelerate the transition from Low to Moderate and Full Circular Mobility, industry players, policymakers and consumers need to work together to implement a series of strategies.

Regulation and policy, support on innovation and further industry collaboration are needed across all 4 Pathways. In Energy Decarbonization:

· We need stronger push from regulatory mandates to phase out ICE sooner than 2030. Many carmakers are still behind in making a shift into alternative powertrains in passenger cars and still lobby regulators to extend ICE and incentives for powertrain variants that are new efficient.

· What’s more, Harmonization of global regulatory requirements could help provide clarity and guidance for the decarbonization roadmaps.

· Policy to promote clean energy is also important, from supply chain to production, and re-use. A complete shift to renewable energy and energy-grid integration could help achieve climate goals faster and contribute to energy security.

In Materials Circularity:

· Players explore recycled components, renewable raw materials, and high-performance polymers for Green Mobility. Applications expand from seats and displays to lighting, roofs, and EV battery packaging.

· We need to move from a linear to a circular value chain of batteries which can improve both the environmental and the economic footprint of batteries by getting more out of batteries while in use, and by harvesting end-of-life value from batteries.

· There is a need to harmonize EV Battery Recycling and 2nd battery life We need to increase the Utilization of Vehicles to achieve higher sustainability by

· Promoting shared mobility, vehicle-on-demand, and mobility-on-demand services as alternatives to vehicle ownership that has low vehicle utilization. Numerous studies have shown that shared mobility (car-sharing, ride-hailing, multi-modal transport) can contribute to sustainability.

· By introducing purpose-made solutions, such as electric, autonomous, and shared taxis made specifically for ride-hailing using renewable energy.

Finally, the last piece of the puzzle is the Optimization of the Vehicle Lifetime.

· New trends are emerging, such as “NO-ownership” or the decision not to own material stuff, vehicles preferring pay-per-use service models, and so on. We are at the beginning a revolution, however it has already started to change our habits, and help cities in reducing their carbon footprint. Although traditional vehicle ownership business models are not threatened yet, we are already consuming mobility as a service, in different forms, for different mobility scenarios. Carmakers are trying new ways to sell cars to younger generations, leveraging “pay as you go models.

· Car subscription business models which offer an alternative to owning or leasing are being introduced by major brands – not only premium ones. And they are expanding from major cities to cover key car markets and include a broad range of vehicle fleet.

· Digitization of the supply chain becomes a critical part of Optimized vehicle lifetime. The benefits are better traceability, agility and better transparency for the sustainable materials used for vehicle production.

What do you envision your industry looking like 10 years from now?

The future of the automotive industry, as well as any other industry, will be determined by the demand (consumers) and supply. The automotive industry is undergoing tremendous change due to increasing urbanization, digitalization, and environmental change. The goal is to reach zero road deaths – hence the transition from manual to autonomous driving, carbon neutrality (through circular mobility) and optimized access via multi-modal mobility on demand.

There are three forces to watch:

1. the impact of regulation on the industry’s roadmaps. Electrification, decarbonization and sustainability are driven by environmental mandates (emission regulations, battery recycling), rather than competition among players.

2. the speed of innovation. Breakthroughs that remove the technological barriers of electrification, such as battery energy density, fast charging, green hydrogen cost could accelerate sustainability. What’s more, innovative business models are disrupting the way the industry works, e.g. Tesla’s electrification strategy and software-over the air updates.

3. and the shift of consumer preferences, e.g., more and more young customers are concerned about the use of animal products in cars and the welfare of animals.

Consumer preferences will shape new products, such as new experiences in the vehicle interior. I’m optimistic that in 2030 the automotive industry will look very different, from the way people move, to what the experience is like and who delivers it.

Here are some changes I’m expecting from the point of the customers / users.

· Vehicle automation will make roads and vehicle safer, but it also promises to “give back” the valuable time lost in mundane commute. Audi calculates that self-driving cars could give back to drivers about 50 minutes per day spent behind the wheel, calling their initiative the 25th hour. I’m expecting that Level 4 autonomy will have expanded from shared mobility (e.g. Waymo) to private ownership by 2030.

· Digitalization of vehicle interface unlocks a new level of services and personalization. We are in the middle of a paradigm shift in driver and passenger experience driven by the speed of innovation in artificial intelligence, big data analytics and cloud computing. Humanized AI and empathetic machines have already entered vehicle cockpits, and they are being trained to build emotional intelligence. With the proliferation of Connected-to-the-car devices and in-vehicle wireless connectivity, occupants can now enjoy an abundance of communication and infotainment services, while remaining “Connected” to the “virtual life” within the vehicle.

· Shared mobility sets new requirements for vehicle security. The convergence of autonomous, electrified and shared mobility promises greater vehicle utilization with new business models emerging such as car-sharing and driverless taxis. However, it will require a new level of vehicle security, for example driver authentication using biometric identification or blockchain in car sharing. Additionally, robust security-by-design is also required to protect against remote hacking. Finally, shared mobility offers significant opportunities for further personalized experience, e.g. for easy access to preferred settings or by automatically configuring seats for mobility services.

· E-mobility might shift unique selling points from 2022 onwards, with passenger wellness and service personalization substituting driver experience and ownership status. Powertrain electrification not only enables a quitter and more relaxing interior but can also help shift customer perception about the USPs of the vehicle and cockpit of the future, e.g. from HP to kWh and range, depending on the segment.

· Data will be the fuel of new business models: While automated and connected driving, electrified powertrains and shared economy form the foundation of the New mobility era, the glue that binds future mobility together is the pursuit for new business models. Mobility-as-a-Service (MaaS), Automated-Mobility-on-Demand (AMoD), Cloud-based Connected Car Services, Vehicle Data Monetization and Mobility Blockchain are some of the emerging business models aiming at creating new value propositions by tackling challenges such as cost, road safety, efficiency and passenger comfort.

· Urban Air Mobility for commercial (flying taxis) and private use cases (private drones) will become a reality within the next decade. Vertical Mobility is a system that enables on-demand, highly automated, passenger or cargo-carrying air transportation services within and around a metropolitan environment. Regulations and airspace management are crucial things for unlocking the potential of UAM disruptive market.

The shift of mobility from a product (e.g., car ownership) to a service (e.g. car sharing) leads to the rise of the role of software vs. hardware. This will lead to the transformation of the ecosystem with new players with expertise in AI and software leading the race. The era of the software-defined vehicle will lead to further transformation of vehicle design, engineering, manufacturing and lead to new car brands, new suppliers emerging as leaders in new mobility.

What can the average person do to make a difference?

We shouldn’t underestimate the impact of individual action as a driver of change. Of course, we need industry regulation, standards and policies to move the needle, but the average person’s decisions and behaviour matter as well.

Choosing products that support ethical sourcing, sustainable production, recycling, 2nd life and optimization of product lifetime can take us one step farther on the path to circularity. As innovation progresses to offer alternatives that would not require a cost premium, the decision to support sustainable solutions will become more and more obvious.

Georgios, thank you for chatting with us and sharing your vision for shifting to a more circular economy in order to meet climate change goals.

Dylan Welch is the CEO and Host of Going Green, a podcast, website, and social media brand that highlights renewable energy, cleantech, and sustainable news.